Skip to content

Skip to content F-tax

Register for F-tax and preliminary taxes

When you start your company, you must register with the Swedish Tax Agency for F-tax. Your business pays F-tax on its income and it is a requirement for being able to run a business. Once you have registered your business, you will receive a preliminary tax based on the expected profit that you specify in your registration. You can update your preliminary income tax return several times during the year if you wish, but it is important to remember that you must pay your preliminary tax every month. If you are unsure about the expected surplus, we recommend being cautious and entering a lower conservative estimate, and rather update the preliminary tax later in the year. Then you don’t have to strain the company’s cash flow with larger tax payments than the income corresponds to.

F-tax and A-tax

It may seem unfortunate and confusing that F-tax can refer to two different things. Either preliminary tax or F-tax slip. Employees in Sweden have a so-called A-tax slip. You have that when you have income as an employee. In order for a company to be allowed to do business, it needs to register for an F-tax slip, which applies to all types of companies. When you start a sole trader firm, you can have both income from business activities and employment, and then you need an FA-tax slip.

Change your F-tax through a preliminary income tax return

If you do not submit a preliminary income tax return for the year, the Tax Agency automatically determines your preliminary tax based on the previous year’s tax. This may mean that you pay too much or too little in preliminary tax, depending on whether your income has changed. Therefore, it is important to update your preliminary income tax return if your income has changed considerably.

If you submit an updated preliminary income tax return during the year, the amount you need to pay in preliminary tax can either change or you can get tax back if you have already paid too much. This can be particularly important if your company’s operations have changed during the year and your income has decreased or increased a lot.

When the final tax is determined for the year, the preliminary tax paid is deducted. If you have paid too much preliminary tax, you will receive a tax refund. If you have paid too little preliminary tax, you must pay residual tax.

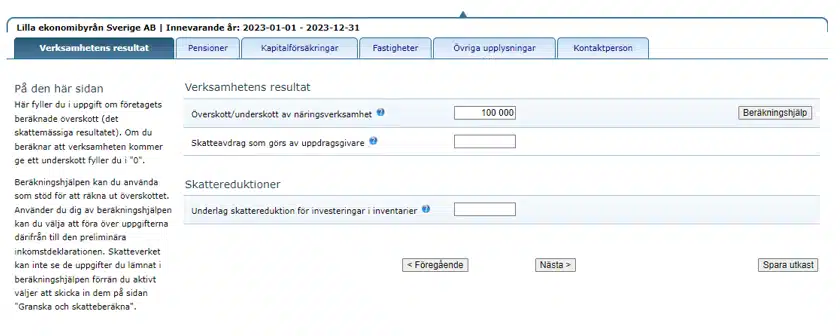

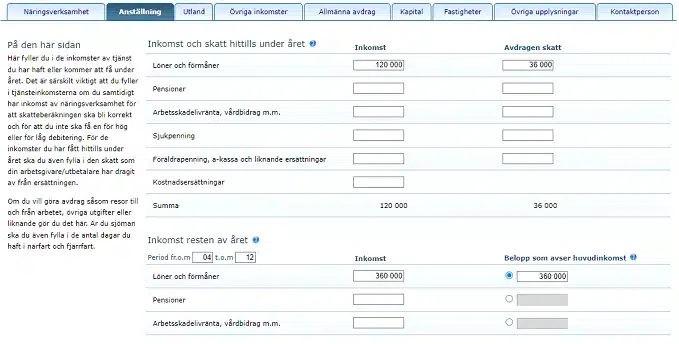

The preliminary income tax return for a limited company is relatively simple as the F-tax is usually only based on expected profit, and pension savings if applicable. For sole trader firms it is more complex, because the F-tax is then based on your entire personal finances and not just on the profit in the company. The form can feel like a jungle because there are so many fields you can fill in, but in practice not that many fields are normally used. For most people, it is enough to state the expected surplus from the sole trader firm, tax and income from employment (Salary from other employers) so far and the rest of the year, and possibly paid interest if you have large mortgages. The preliminary income tax return does not have to be exact, as it is only a matter of obtaining an approximate figure to pay each month so that the tax payments during the year will end up as close as possible to the final tax.

For most limited companies, only the surplus/deficit of business activities needs to be stated in the preliminary income tax return. If your company also has pension costs, you need to fill them in in the tab for pensions.

Sole trader firms must also state surplus/deficit from business activities, but if you also have income from employment during the year, you must also state figures for that.

Frequenty Asked Questions about F-tax and preliminary income tax returns

How could I know what the expected surplus is when I have just started the company?

It’s obviously impossible to know, so just make the best guess you can and round it down. If it turns out that the guess was incorrect, you can either submit a preliminary income return to update the preliminary tax, or leave it be and settle the tax via the final tax statement.

Do I have to submit a preliminary income tax return?

There is no requirement to submit a preliminary income declaration in addition to the one submitted when registering the company. However, it is recommended to do so if the expected surplus changes significantly from what was previously registered.

Why does it feel like I pay much more tax with a sole trader firm than as an employee?

The tax, and therefore also the preliminary tax, in a sole trader firm is both for income tax and personal tax contributions. The personal tax contributions are the sole trader firm’s equivalent to employer taxes for normal employments. The employer taxes are not noticed as an employee because it is the employer who handles them. All in all, there will be approximately the same amount of tax in both cases.

Summary

Preliminary tax is a monthly advance payment of expected tax for the year. If necessary, you can adjust your preliminary tax by submitting a preliminary income tax return. If you pay too much preliminary tax, you will get a tax refund and if you pay too little, you will have to pay more tax when the final tax is determined.