Skip to content

Skip to content Even if a sole trader business is intended to be a simple form of company, it is, as we see it, the most difficult form of company to understand how taxes work.

The main reason why it is difficult to understand is that taxes work so differently compared to salaries from regular employment that most people are familiar with. If you have a limited company, you deduct tax for each salary payment, and then pay that tax and the employer’s contribution the following month. In a sole trader business, you do not pay tax on your withdrawals, but you pay tax on the profit that you declare at the end of the year.

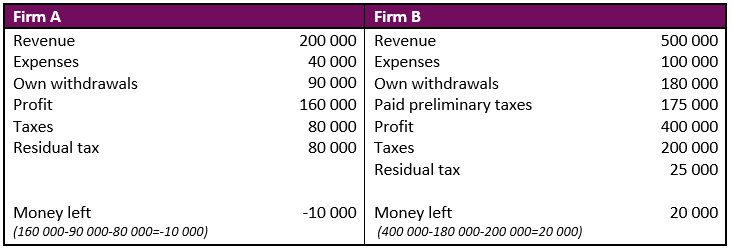

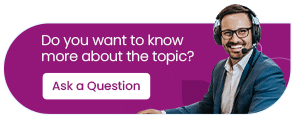

So the money you deposit or withdraw from your company does not affect your tax. To make it easier to understand, we here provide some simplified examples of calculations.

So the money you deposit or withdraw from your company does not affect your tax. To make it easier to understand, we here provide some simplified examples of calculations.

So the money you deposit or withdraw from your company does not affect your tax. To make it easier to understand, we here provide some simplified examples of calculations.